In The Money

CPF and SRS dos and don’ts for the year end

This fortnightly column addresses readers’ investing issues.

Q: It’s nearly the end of the year. If I haven’t done anything on the Central Provident Fund or Supplementary Retirement Scheme (SRS) front, are there any tips on what I should do?

Central Provident Fund is a key area of your finances that should not be neglected. Topping up the various accounts will boost your retirement funds and give you some tax relief. CPF is an effective instrument to reap the benefits of compounding over the long run, says DBS Bank head of financial planning literacy Lorna Tan.

Interest rates on the various CPF accounts have not changed, even though interest rates in general have been rising.

The CPF Board said last week that “the Government is watching the interest rate environment closely to ensure that the CPF interest rate pegs remain relevant in the prevailing operating environment while taking into consideration the longer-term outlook”.

Tip 1: Top up your CPF accounts

Below 55 years of age: top up CPF Special Account (SA)

Top up your retirement funds by contributing to the SA. The limit is the current Full Retirement Sum (FRS) less the sum of SA and the amount withdrawn from SA for investment.

Assume you have $80,000 in the SA comprising $40,000 cash and $40,000 in unit trusts. As the FRS is $192,000 this year, this means that you can top up your SA by $112,000 ($192,000 minus $80,000).

Above 55 years of age and topping up of Retirement Account (RA)

Your RA is created when you hit 55. The top-up limit is the Enhanced Retirement Sum ($288,000 this year) less RA savings.

As an illustration, under the CPF Life Standard Plan, if you have the Full Retirement Sum of $192,000 in your RA by 55, you will be able to receive a monthly payout of between $1,470 and $1,570 from 65.

If you top up your RA to the current maximum of $288,000, you could get the higher monthly payouts of an estimated $2,140 to $2,300 via CPF Life when you reach 65.

Topping up of MediSave Account (MA)

You can top up your MA up to the Basic Healthcare Sum (BHS), which is $66,000 this year. CPF has just announced that the BHS will be $68,500 next year.

Tip 2: Enjoy tax relief on your topping-up sums

Topping-up your own CPF accounts

You get to enjoy tax relief of up to $8,000 (previously $7,000) per calendar year when you top up your SA, RA and/or MA.

Do note that there is no tax relief when you top-up your RA beyond the Full Retirement Sum, said PhillipCapital financial services manager Elijah Lee.

Topping-up of loved ones’ CPF accounts

There is an additional tax relief of up to $8,000 (previously $7,000) when you top up your loved ones’ SA, RA and/or MA. Loved ones could be parents, parents-in-law, grandparents, grandparents-in-law, spouse and siblings.

However, for a spouse or sibling, you will be eligible for the tax relief only if his/her income in the previous year does not exceed $4,000 or if the recipient is handicapped.

Tip 3: Timing of top-up

DBS’ Ms Tan suggests performing the top-ups at the start of the year to earn more interest.

As CPF interest is computed monthly, topping up your CPF accounts in January rather than December could earn 20 per cent more interest over 10 years.

PhillipCapital’s Mr Lee noted that those whose income is variable may wish to do a one-time top-up closer to the end of the year when they have a better picture of their overall income for the year.

Tip 4: Transfer funds from the CPF Ordinary Account to the SA

This is not necessarily something you need to do before the end of the year, but it is worth considering to maximise the return on your funds.

Mr Samuel Rhee, chairman and chief investment officer of digital wealth adviser Endowus, suggests that younger CPF members with low CPF SA and MA balances can transfer funds from the OA to SA to enjoy the higher CPF interest rate of 4 per cent a year.

Mr Lee said that for some of his younger clients who have been doing such regular transfers, there is a risk that their OA may end up being insufficient for a downpayment on a property if they have not planned ahead.

“Identify the timing of your property purchases to ensure you will have sufficient OA funds for such big-ticket transactions,” he added.

How to top up your CPF

– Download the CPF forms and fill them up or

– For the CPF mobile app, log in using your Singpass, tap on menu icon and choose “Services”. Choose “Cash Top-up” and indicate the recipient (“Self” or “Loved Ones”), submit your application, and make payment immediately or

– For the CPF website, go to cpf.gov.sg/rstuform and log in using your Singpass. Choose your preferred cash top-up method and top up via PayNow QR, eNETs or via Giro.

What is SRS?

The Supplementary Retirement Scheme (SRS) is a voluntary scheme to encourage individuals to save for retirement and to supplement their CPF savings. It was introduced in 2001.

The yearly maximum SRS contribution from Singapore citizens and permanent residents is $15,300 and $35,700 for foreigners.

Contributions to SRS are eligible for tax relief. You get a dollar-for-dollar tax relief on your SRS contributions, which reduces your chargeable income.

All SRS contributions must be made by Dec 31 of the year or as your SRS operator requires, to be eligible for SRS tax relief in the following year of assessment, said DBS’ Ms Tan.

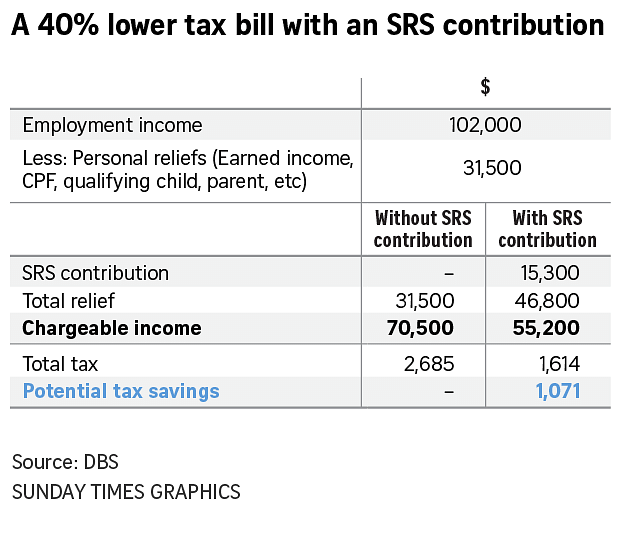

See the calculation in the table for how making an SRS contribution for the year can bring down your tax bill.

Tip 1: Don’t leave funds idle in the SRS account

Ms Tan advises people not to let the cash in the SRS account remain idle after you have moved funds there. The interest paid currently stands at 0.05 per cent per annum.

A significant 24 per cent of total SRS contributions ($14.36 billion), or $3.44 billion, were left idle as at end December 2021, she added.

Funds in the SRS account can be invested in many different types of investment products ranging from fixed deposits, government bonds and securities to insurance, shares and unit trusts.

Applications for Singapore Government Securities bonds and Treasury-bills and the popular Singapore Savings Bonds can be made through the Internet banking portals of your SRS operator (DBS/POSB, OCBC or UOB).

All profits made from investing your SRS contributions will return to your SRS account.

Tip 2: Keep an eye on the tax relief cap

The personal income tax relief cap of $80,000 a year applies.

If a high-income working mother has two children or more, the numbers may not work out for her to contribute to SRS if her Working Mother Child Relief claims are significant, noted PhillipCapital’s Mr Lee.

Tip 3: Pay attention to the timing of SRS withdrawals

The penalty-free 10-year withdrawal period starts from the statutory retirement age that was prevailing at the time of your first SRS contribution.

Only 50 per cent of withdrawals (post statutory retirement age) are taxable. So, to reduce your tax burden, stagger your withdrawals, advises Ms Tan.

Example:

A Singapore resident has an SRS balance of $400,000. He withdraws $40,000 each year (over 10 years). This means that 50 per cent of that amount, or $20,000, will be taxable each year.

If he has no other source of taxable income, he will not need to pay any income tax as the first $20,000 of total annual income is tax-exempted.

Note that SRS withdrawals need not be in cash. This means being able to hold onto the SRS investments instead of having to liquidate them first before withdrawing them in cash.

Tip 4: Pay attention to the various fees charged when investing

Instead of setting aside a lump sum once a year, you can make regular monthly transfers to your SRS account up to the annual tax-relief limit. Pay attention to costs such as transaction fees, sales fees or trailer fees when investing, said Endowus’ Mr Rhee.

Bottom line

If you have not done the various top-ups and you are able to spare the funds, do so in order to claim tax relief for the income you have earned this year.

Investment involves risk. Past performance is not necessarily a guide to future performance or returns.

The value of investments and the income from them can go down as well as up, and you may not get back the full amount you invested.

If you are in doubt, you should consult your stockbroker, bank manager, solicitor or other professional advisers.

Join ST's Telegram channel and get the latest breaking news delivered to you.

No comments:

Post a Comment