Increase in voluntary CPF top-ups; national survey showed more awareness of retirement planning

SINGAPORE – Singaporeans are beefing up their retirement nest eggs, with voluntary top-ups to CPF accounts hitting more than $3 billion in the first eight months of the year.

The figure was up 15 per cent on the same period in 2023, noted the Central Provident Fund (CPF) Board on Oct 2.

Voluntary top-ups refer to cash and CPF transfers made to the Special Account (SA) of members aged below 55 or to the Retirement Account (RA) of those above 55.

CPF members can make these contributions for themselves or for their family members to ensure higher monthly payouts in retirement.

Every dollar a member contributes yields a dollar in tax relief, up to $16,000 a year. The top-ups must be made by Dec 31.

The tax relief comprises $8,000 for top-ups to a member’s own SA, and an additional $8,000 for top-ups for family members such as parents, parents-in-law, grandparents, spouse and siblings.

The increased voluntary contributions to the CPF in the eight months to Aug 31 come as a survey commissioned by the Ministry of Manpower (MOM) indicated a greater awareness of retirement planning among Singaporeans.

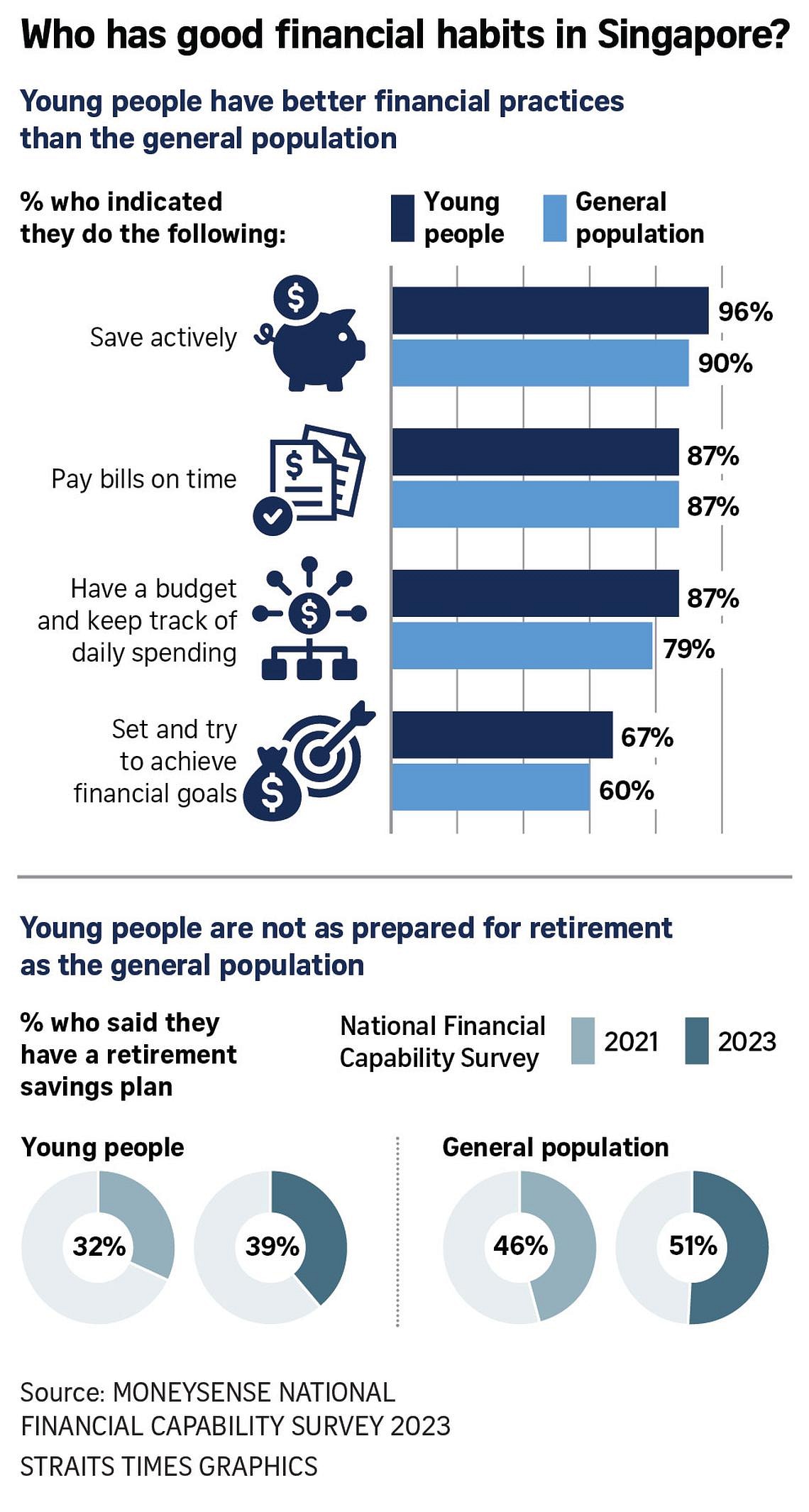

It found that 51 per cent of those polled in 2023 had developed a retirement savings plan, up from 46 per cent when the same survey was first conducted in 2021.

About 40 per cent of those aged 18 to 35 had planned for retirement, up from the 32 per cent in 2021.

A nationally representative sample of 2,000 residents aged 18 to 79 were polled between July and September in 2023.

While there was an improvement from 2021, the survey showed that more people could still take steps to start retirement planning earlier.

Other findings indicate that Singapore residents generally have good money management habits, with 90 per cent saving actively and almost 90 per cent paying their bills on time. About 80 per cent kept track of their daily spending, and 70 per cent had set aside at least three months of expenses for emergency needs.

Young people displayed better financial behaviour, the survey found. It noted that 96 per cent saved actively, higher than the 90 per cent among the general population. And 87 per cent had a budget and kept track of their daily spending, compared with 79 per cent of the general population.

Mr Jeremy Huang, director of MOM’s financial planning programme department, said the ministry will continue to work with the CPF Board to help Singaporeans make well-informed financial decisions and prepare for retirement.

To this end, the CPF Board and MoneySense, the national financial education programme, are running a retirement planning campaign for the second consecutive year.

Ms Peh Er Yan, group director for the communications and engagement division at the CPF Board, said the goal is to encourage Singaporeans to take small actions today to improve their financial health and plan for retirement.

“By instilling good financial habits, we hope to support Singaporeans to navigate key life moments with financial calm,” she added.

Some simple financial habits include having a pot of savings, budgeting for big-ticket items such as a home, having adequate health insurance and planning for retirement.

Mr Law Jia Hong, 30, a manager, said it is important to build up savings for a rainy day.

He finds simple ways to do so by using discounts wisely and by assessing the costs and benefits before making a purchase. Mr Law also sets aside a daily budget and sticks to it, so he does not overspend.

Content writer Suphon Liao, 32, set aside a budget for his house. While waiting for the keys, he parked the money in safe investments such as fixed deposits or Treasury bills to earn some interest.

He also scoured the internet for tips so that he could design his home on his own and save on interior design fees.

Madam Devikala Somasundaram, 42, could fall back on her health savings and insurance when her daughter was hospitalised.

The savings in her MediSave took care of the initial bill, while the remaining amount was covered by national insurance scheme MediShield Life.

Having adequate savings and health insurance meant that the senior assistant manager did not have to pay from her own pocket, which would have affected her financial plans.

It also allowed her to focus on caring for her daughter without having to worry about the bills.

Retiree Betty Lynn Wong, 59, planned for her retirement by making sure that her savings were sufficient to meet her needs. She also regularly reviews her financial situation to ensure that she has enough to maintain her lifestyle.

The campaign by the CPF Board and MoneySense runs until Dec 31. There will be a Ready for Life Festival on Nov 2 that will feature talks and activities to guide participants on retirement planning.

Join ST's Telegram channel and get the latest breaking news delivered to you.

No comments:

Post a Comment