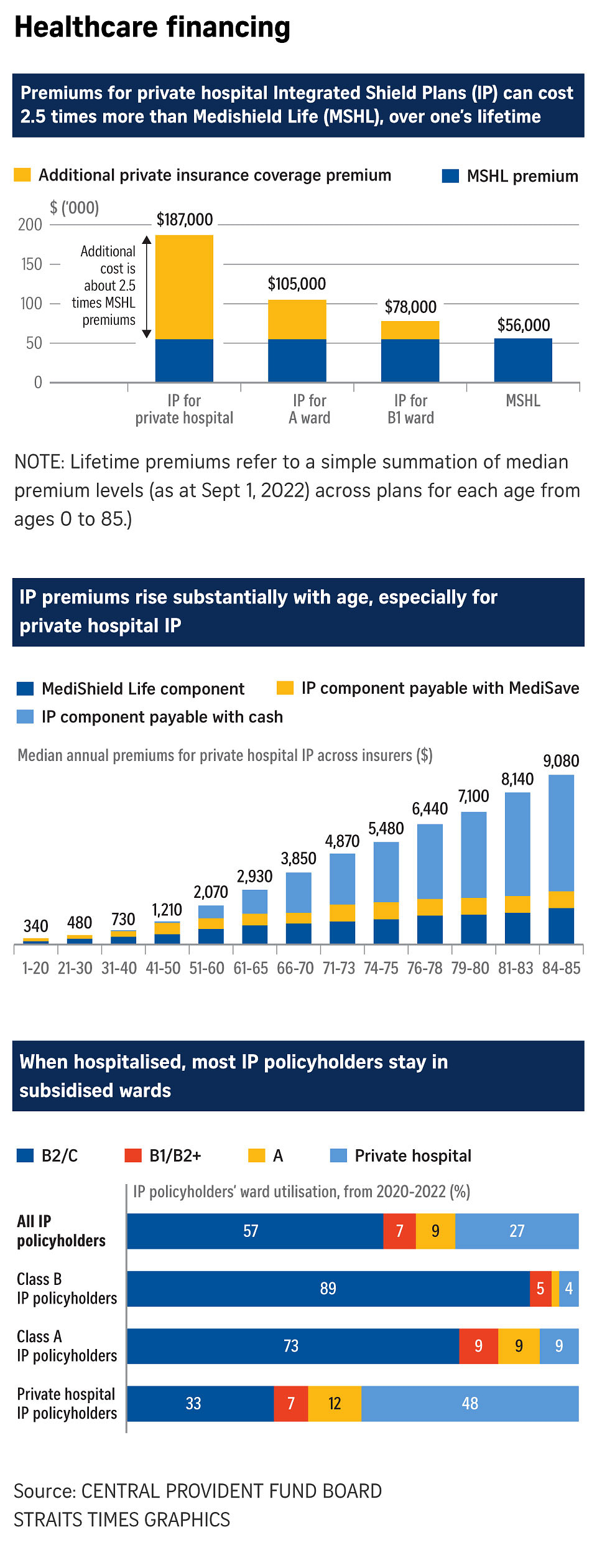

More than half who buy IPs for private healthcare opt for subsidised wards when hospitalised

SINGAPORE – Almost three million people here have Integrated Shield plans (IPs) that pay for private care in hospitals.

Yet more than half opt for subsidised care when they are hospitalised.

The latest data on the Central Provident Fund (CPF) Board’s healthcare financing website show that from 2020 to 2022, 57 per cent of Singaporeans and permanent residents – who had paid for higher coverage with IPs that complement their MediShield Life basic health insurance – had chosen subsidised wards.

Of those who bought the most expensive, private hospital IPs, less than half actually sought treatment at a private hospital.

Associate Professor Jeremy Lim of the NUS Saw Swee Hock School of Public Health said: “Individuals have different states of mind when purchasing insurance and when actually using it. At time of purchase, maximum coverage with the most optionality is sought.

“Upon actual use, however, especially in these times with co-payments and uncertainty around final bill sizes, they elect to be ‘cautious’ and downgrade.”

Mr Alfred Chia, chief executive officer of financial counselling firm SingCapital, said people may go for private care for some conditions, but turn to subsidised care for chronic problems.

“The IP only pays for the hospital component. If the person requires long term medication or treatment, this comes from their own cash. Opting for subsidised treatment means they continue to pay subsidised rates for the follow-up,” he added.

Mr Chia said many people buy their IPs when they are young and the premiums are low. Since premiums are paid by MediSave, most do not think about it till they reach the age when they need to top up premiums with cash.

He suggested people review their IP regularly to see if it still fits their health and financial profile.

For the 70 per cent of people with IPs, the cost is paid for with MediSave money subject to age-related caps. Premiums that are higher than the caps have to be paid for in cash.

Based on the median annual payment for private hospital IPs, more than half the premiums will need to be paid for in cash from the time someone is in his late 60s.

By the time they are in their 80s, the cash component of the premium would likely exceed $5,000 a year.

The board advised: “Before you purchase an IP, it is essential to consider the coverage that you need and its long-term affordability.”

Based on current premium rates, it said someone with an IP pegged at private hospital care would be paying $187,000 in premiums over his or her lifetime – and this does not take into account premium increases in the future.

In contrast, someone who sticks to just MediShield Life, the mandatory national medical insurance, would pay less than a third in premiums – an estimated $56,000 over his or her lifetime.

The two million people who have riders that pay the bulk of their portion of the bill need to pay additional premiums, also with cash.

The Ministry of Health (MOH) insists that an initial amount of between $1,500 and $5,250 a year be paid by the patient before insurance kicks in. On top of that, a patient still has to pay 3 to10 per cent of the remainder of the bills

Riders cover the bulk of this, with most patients paying no more than $3,000 a year.

The CPF Board said the basic MediShield Life, together with MediSave, completely cover the bills for 70 per cent of subsidised Singaporean patients.

Of the rest, a third need to pay $100 or less in cash, another third pay $100 to $500, and the rest pay more than $500.

The board noted that while IPs cost more, “they may not give higher payouts for hospitalisation in B2 and C wards”.

Patients in B2 and C class wards at public hospitals get 50 to 80 per cent subsidy if they are Singaporean, and 25 to 50 per cent if they are PRs, based on means testing.

“Consider if paying for IP premiums is an efficient use of your MediSave. Your savings in your MediSave Account can earn an attractive interest rate of 4 per cent per annum, which can help to meet your future healthcare needs,” the CPF Board said.

Prof Lim agreed that it would make economic sense for some people to buy a lower-tiered plan.

But he said more needs to be done, such as sharing of actual data, in order to overcome this “inherent contradiction in behaviour”.

Read the full story for $0.99/month

Save more than 90% on your subscription and get over 500 subscriber-only articles every month.

ST All-Digital Package - Monthly

$29.90 $0.99/month

No contract

$0.99/month for the first 3 months, $29.90/month thereafter. T&Cs apply.

Unlock these benefits

Get subscriber-only articles on ST Web and app

Easy access on up to 4 devices

2-week e-paper archive to ensure you never miss out on news that matters to you

Join ST's WhatsApp Channel and get the latest news and must-reads.

No comments:

Post a Comment