Demand for the latest tranche is down

Published Thu, Apr 25, 2024 · 01:31 PM

Add happy years to healthy life and healthy life to happy years. Your food becomes your body.Your thoughts become your words.Your words become your actions.Your actions become your habits.Your habits form your characters.Your characters decide your destiny.This blog serves as a platform for exchange of ideas for healthy eating and healthy living.

Note: According to the Singapore Health Promotion Board, a Healthy BMI is greater than18.5 and less than 23.0. A BMI less than 18.5 would mean that the individual is at risk of nutrition deficiency diseases and osteoporosis.

A BMI equal or greater than 23.0 would mean that the individual is at risk of obesity-related diseases. (Ref: DD-Md2022J28)

As of 2024-04-28,

Note: ### indicates BMI = 23 or > 23

Total number of Monthly Weight monitored was 203 (100%)

The no. of times my healthy BMI between 18.5 and 22.9 was 198 (97.536%)

The no. of times my unhealthy BMI equal or more than 23.000 was 5 (2.464%)

=======================

2007

2007-05-28 morning, my weight = 65.0 kg, BMI = 23.588###

2007-06-28 morning, my weight = 61.0 kg, BMI = 22.136

2007-07-28 morning, my weight = 59.0 kg, BMI = 21.410

2007-08-28 morning, my weight = 58.7 kg, BMI = 21.302

2007-09-28 morning, my weight = 57.5 kg, BMI = 20.866

2007-10-28 morning, my weight = 57.5 kg, BMI = 20.866

2007-11-28 morning, my weight = 56.2 kg, BMI = 20.394

2007-12-28 morning, my weight = 55.5 kg, BMI = 20.140

2008

2008-01-28 morning, my weight = 54.8 kg, BMI = 19.886

2008-02-28 morning, my weight = 54.8 kg, BMI = 19.886

2008-03-28 morning, my weight = 54.5 kg, BMI = 19.777

2008-04-28 morning, my weight = 54.4 kg, BMI = 19.741

2008-05-28 morning, my weight = 54.1 kg, BMI = 19.632

2008-06-28 morning, my weight = 54.6 kg, BMI = 19.814

2008-07-28 morning, my weight = 54.5 kg, BMI = 19.777

2008-08-28 morning, my weight = 54.3 kg, BMI = 19.705

2008-09-28 morning, my weight = 54.9 kg, BMI = 19.923

2008-10-28 morning, my weight = 55.3 kg, BMI = 20.068

2008-11-28 morning, my weight = 54.5 kg, BMI = 19.777

2008-12-28 morning, my weight = 55.6 kg, BMI = 20.177

2009

2009-01-28 morning, my weight = 54.8 kg, BMI = 19.886

2009-02-28 morning, my weight = 55.9 kg, BMI = 20.285

2009-03-28 morning, my weight = 54.8 kg, BMI = 19.886

2009-04-28 morning, my weight = 55.3 kg, BMI = 20.068

2009-05-28 morning, my weight = 55.4 kg, BMI = 20.104.

2009-06-28 morning, my weight = 55.2 kg, BMI = 20.031

2009-07-28 morning, my weight = 55.1 kg, BMI = 19.995

2009-08-28 morning, my weight = 55.2 kg, BMI = 20.031

2009-09-28 morning, my weight = 56.3 kg, BMI = 20.431

2009-10-28 morning, my weight = 55.8 kg, BMI = 20.249

2009-11-28 morning, my weight = 56.2 kg, BMI = 20.394

2009-12-28 morning, my weight = 56.1 kg, BMI = 20.358

2010

2010-01-28 morning, my weight = 55.6 kg, BMI = 20.177

2010-02-28 morning, my weight = 56.5 kg, BMI = 20.503

2010-03-28 morning, my weight = 56.4 kg, BMI = 20.467

2010-04-28 morning, my weight = 55.7 kg, BMI = 20.213

2010-05-28 morning, my weight = 55.1 kg, BMI = 19.995

2010-06-28 morning, my weight = 56.4 kg, BMI = 20.467

2010-07-28 morning, my weight = 55.5 kg, BMI = 20.140

2010-08-28 morning, my weight = 55.8 kg, BMI = 20.249

2010-09-28 morning, my weight = 55.8 kg, BMI = 20.249

2010-10-28 morning, my weight = 55.4 kg, BMI = 20.104

2010-11-28 morning, my weight = 55.6 kg, BMI = 20.177

2010-12-28 morning, my weight = 55.5 kg, BMI = 20.140

2011

2011-01-28 morning, my weight = 55.4 kg, BMI = 20.104

2011-02-28 morning, my weight = 56.5 kg, BMI = 20.503

2011-03-28 morning, my weight = 55.6 kg, BMI = 20.177

2011-04-28 morning, my weight = 55.7 kg, BMI = 20.213

2011-05-28 morning, my weight = 55.6 kg, BMI = 20.177

2011-06-28 morning, my weight = 56.3 kg, BMI = 20.431

2011-07-28 morning, my weight = 56.5 kg, BMI = 20.503

2011-08-28 morning, my weight = 56.9 kg, BMI = 20.649

2011-09-28 morning, my weight = 56.2 kg, BMI = 20.394

2011-10-28 morning, my weight = 56.8 kg, BMI = 20.613

2011-11-28 morning, my weight = 59.0 kg, BMI = 21.410

2011-12-28 morning, my weight = 60.3 kg, BMI = 21.882

2012

2012-01-28 morning, my weight = 61.5 kg, BMI = 22.318

2012-02-28 morning, my weight = 62.7 kg, BMI = 22.753

2012-03-28 morning, my weight = 62.5 kg, BMI = 22.681

2012-04-28 morning, my weight = 61.3 kg, BMI = 22.246

2012-05-28 morning, my weight = 60.7 kg, BMI = 22.028

2012-06-28 morning, my weight = 60.6 kg, BMI = 21.992

2012-07-28 morning, my weight = 61.2 kg, BMI = 22.209

2012-08-28 morning, my weight = 60.8 kg, BMI = 22.064

2012-09-28 morning, my weight = 61.5 kg, BMI = 22.318**

2012-10-28 morning, my weight = 62.3 kg, BMI = 22.608

2012-11-28 morning, my weight = 63.4 kg, BMI = 23.008###

2012-12-28 morning, my weight = 62.9 kg, BMI = 22.826

2013

2013-01-28 morning, my weight = 63.0 kg, BMI = 22.863

2013-02-28 morning, my weight = 62.1 kg, BMI = 22.536

2013-03-28 morning, my weight = 61.5 kg, BMI = 22.318

2013-04-28 morning, my weight = 63.1 kg, BMI = 22.899****

2013-05-28 morning, my weight = 62.3 kg, BMI = 22.608

2013-06-28 morning, my weight = 62.2 kg, BMI = 22.572

2013-07-28 morning, my weight = 62.4 kg, BMI = 22.645

2013-08-28 morning, my weight = 62.6 kg BMI = 22.717

2013-09-28 morning, my weight = 62.4 kg BMI = 22.645**

2013-10-28 morning, my weight = 62.3 kg BMI = 22.609

2013-11-28 morning, my weight = 63.1 kg BMI = 22.899

2013-12-28 morning, my weight = 64.4 kg BMI = 23.371###

2014

2014-01-28 morning, my weight = 63.6 kg, BMI = 23.080###

2014-02-28 morning, my weight = 63.3 kg, BMI = 22.971

2014-03-28 morning, my weight = 62.7 kg, BMI = 22.753

2014-04-28 morning, my weight = 62.7 kg, BMI = 22.753

2014-05-28 morning, my weight = 62.9 kg, BMI = 22.826

2014-06-28 morning, my weight = 63.1 kg BMI = 22.899

2014-07-28 morning, my weight = 62.7 kg, BMI = 22.753

2014-08-28 morning, my weight = 62.2 kg, BMI = 22.572

2014-09-28 morning, my weight = 61.2 kg, BMI = 22.209

2014-10-28 morning, my weight = 61.4 kg, BMI = 22.282

2014-11-28 morning, my weight = 60.2 kg, BMI = 21.846

2014-12-28 morning, my weight = 60.8 kg, BMI = 22.064

2015

2015-01-28 morning, my weight = 61.3 kg, BMI = 22.246

2015-02-28 morning, my weight = 61.8 kg, BMI = 22.427

2015-03-28 morning, my weight = 61.8 kg, BMI = 22.427

2015-04-28 morning, my weight = 62,5. kg, BMI = 22.681

2015-05-28 morning, my weight = 62.4 kg, BMI = 22.645

2015-06-28 morning, my weight = 63.6 kg, BMI = 23.080###

2015-07-28 morning, my weight = 62.3 kg BMI = 22.609

2015-08-28 morning, my weight = 62.2 kg, BMI = 22.572

2015-09-28 morning, my weight = 63.0 kg, BMI = 22.863

2015-10-28 morning, my weight = 63.2 kg, BMI = 22.935

2015-11-28 morning, my weight = 62.6 kg, BMI = 22.717

2015-12-28 morning, my weight = 62.3 kg BMI = 22.609

2016

2016-01-28 morning, my weight = 63.0 kg, BMI = 22.863

2016-02-28 morning, my weight = 62.8 kg, BMI = 22.790

2016-03-28 morning, my weight = 62.0 kg, BMI = 22.499

2016-04-28 morning, my weight = 62.0 kg, BMI = 22.499

2016-05-28 morning, my weight = 62.4 kg, BMI = 22.645

2016-06-28 morning, my weight = 62.1 kg, BMI = 22.536

2016-07-28 morning, my weight = 62.2 kg, BMI = 22.572

2016-08-28 morning, my weight = 62.6 kg, BMI = 22.717

2016-09-28 morning, my weight = 62.8 kg, BMI = 22.790

2016-10-28 morning, my weight = 62,5. kg, BMI = 22.681

2016-11-28 morning, my weight = 62.1 kg, BMI = 22.536

2016-12-28 morning, my weight = 62.3 kg, BMI = 22.608

2017

2017-01-28 morning, my weight = 62.9 kg, BMI = 22.826

2017-02-28 morning, my weight = 62.4 kg, BMI = 22.644

2017-03-28 morning, my weight = 62.8 kg, BMI = 22.789

2017-04-28 morning, my weight = 62.3 kg, BMI = 22.609

2017-05-28 morning, my weight = 62.2 kg, BMI = 22.572

2017-06-28 morning, my weight = 62.6 kg, BMI = 22.717

2017-07-28 morning, my weight = 62.4 kg, BMI = 22.645

2017-08-28 morning, my weight = 61.9 kg, BMI = 22.463

2017-09-28 morning, my weight = 62.0 kg, BMI = 22.499

2017-10-28 morning, my weight = 62.0 kg, BMI = 22.499

2017-11-28 morning, my weight = 61.5 kg, BMI = 22.318

2017-12-28 morning, my weight = 61.5 kg, BMI = 22.318

2018

My Weight 2018-01-28 0934 hr 61.0 kg BMI 22.136

My Weight 2018-02-28 0915 hr 60.7 kg BMI 22.027

My Weight 2018-03-28 0620 hr 61.0 kg BMI 22.136

My Weight 2018-04-28 1005 hr 61.7 kg BMI 22.390

My Weight 2018-05-28 0856 hr 60.5 kg BMI 21.955

My Weight 2018-06-28 0600 hr 61.4 kg BMI 22.281

My Weight 2018-07-28 0600 hr 62.2 kg BMI 22.572

My Weight 2018-08-28 0720 hr 61.4 kg BMI 22.281

My Weight 2018-09-28 0805 hr 62.1 kg BMI 22.535

My Weight 2018-10-28 0750 hr 61.3 kg BMI 22.24

My Weight 2018-11-28 1000 hr 61.5 kg BMI 22.318

My Weight 2018-12-28 0650 hr 62.5 kg BMI 22.681

2019

2019-01-28 at 1000 hr 60.9 kg BMI 22.100

2019-02-28 at 0946 hr 61.0 kg BMI 22.136

2019-03-28 at 0700 hr 62.4 kg BMI 22.644

2019-04-28 at 0828 hr 62.9 kg BMI 22.826

2019-05-28 at 0745 hr 62.4 kg BMI 22.826

2019-06-28 at 0650 hr 62.4 kg BMI 22.644

2019-07-28 at 0736 hr 62.8 kg BMI 22.789

2019-08-28 at 0629 hr 62.4 kg BMI 22.644

2019-09-28 at 0644 hr 61.9 kg BMI 22.463

2019-10-28 at 0740 hr 62.5 kg BMI 22.681

2019-11-28 at 0632 hr 62.8 kg BMI 22.789

2019-12-28 at 0726 hr 62.5 kg BMI 22.681

2020

My Weight 2020-01-28 0625 HR 62.6 kg BMI 22.717

My Weight 2020-02-28 0728 HR 62.3 kg BMI 22.608

My Weight 2020-03-28 0649 HR 61.4 kg BMI 22.281

My Weight 2020-04-28 0810 HR 62.0 kg BMI 22.499

My Weight 2020-05-28 0714 HR 62.3 kg BMI 22.608

My Weight 2020-06-28 0757 HR 60.2 kg BMI 21.846

My Weight 2020-07-28 0715 HR 61.6 kg BMI 22.354

My Weight 2020-08-28 0707 HR 61.1 kg BMI 22.173

My Weight 2020-09-28 0609 HR 60.8 kg BMI 22.064

My Weight 2020-10-28 0818 HR 60.7 kg BMI 22.027

My Weight 2020-11-28 0706 HR 60.9 kg BMI 22.100

My Weight 2020-12-28 0631 HR 60.5 kg BMI 21.955

2021

My Weight 2021-01-28 0638 HR 61.3 kg BMI 22.245

My Weight 2021-02-28 0741 HR 61.2 kg BMI 22.209

My Weight 2021-03-28 0659 HR 61.3 kg BMI 22.245

My Weight 2021-04-28 0659 HR 61.1 kg BMI 22.173

My Weight 2021-05-28 0618 HR 61.1 kg BMI 22.173

My Weight 2021-06-28 0604 HR 61.3 kg BMI 22.245

My Weight 2021-07-28 0642 HR 61.2 kg BMI 22.209

My Weight 2021-08-28 0653 HR 61.5 kg BMI 22.318

My Weight 2021-09-28 0618 HR 61.5 kg BMI 22.318

My Weight 2021-10-28 0549 HR 61.0 kg BMI 22.136

My Weight 2021-11-28 0630 HR 61.3 kg BMI 22.245

My Weight 2021-12-28 0528 HR 61.6 kg BMI 22.354

======================================

2022

My Weight 2022-01-28 0910 HR 61.1 kg BMI 22.173

My Weight 2022-02-28 0642 HR 61.2 kg BMI 22.209

My Weight 2022-03-28 0649 HR 61.4 kg BMI 22.281

My Weight 2022-04-28 0649 HR 61.4 kg BMI 22.281

My Weight 2022-05-28 0549 HR 61.0 kg BMI 22.136

My Weight 2022-06-28 0549 HR 61.0 kg BMI 22.136

My Weight 2022-07-28 0700 HR 60.6 kg BMI 21.991

My Weight 2022-08-28 0640 HR 61.3 kg BMI 22.245

My Weight 2022-09-28 0738 HR 61.7 kg BMI 22.390

My Weight 2022-10-28 0708 HR 61.5 kg BMI 22.318

My Weight 2022-11-28 0706 HR 60.9 kg BMI 22.100

My Weight 2022-12-28 0722 HR 61.1 kg BMI 22.173

========

2023

My Weight 2023-01-28 0537 HR 60.9 kg BMI 22.100

My Weight 2023-02-28 0515 HR 61.4 kg BMI 22.281

My Weight 2023-03-28 0606 HR 61.3 kg BMI 22.245

My Weight 2023-04-28 0738 HR 61.3 kg BMI 22.245

My Weight 2023-05-28 0721 HR 61.0 kg BMI 22.136

My Weight 2023-06-28 0641 HR 61.2 kg BMI 22.209

My Weight 2023-07-28 0700 HR 60.9 kg BMI 22.100

My Weight 2023-08-28 0655 HR 61.3 kg BMI 22.245

My Weight 2022-09-28 0738 HR 61.7 kg BMI 22.390

My Weight 2022-10-28 0708 HR 61.5 kg BMI 22.318

My Weight 2023-11-28 0612 HR 61.4 kg BMI 22.281

My Weight 2023-12-28 0734HR 61.3 kg BMI 22.245

========

2024

My Weight 2024-01-28 0734 HR 61.3 kg BMI 22.245

My Weight 2024-02-28 0510 HR 61.6 kg BMI 22.354

My Weight 2024-03-28 0642 HR 60.9 kg BMI 22.100

My Weight 2024-04-28 0721 HR 61.1 kg BMI 22.173

==================================== ===

Note:

My current BMI is within the healthy range of 18.5 to 22.9.

For me, the range of healthy weight is 50.9786 kg (BMI = 18.5) to 63.10324 kg (BMI = 22.9).

People with BMI values of 23 kg/m2 (or 25 kg/m2 according to some sources) and above have been found to be at risk of developing heart disease and diabetes.

To be healthy, I must have a healthy weight.

Be as lean as possible without being underweight, as recommended by World Cancer Prevention Foundation, United Kingdom.

=================================

Note: On 2021-05-28, I removed the unimportant details of old records from My Weight Management Records.

=================================

Ref. WeightManagement

Demand for the latest tranche is down

THE cut-off yield on the latest Singapore six-month Treasury bill (T-bill) fell slightly to 3.74 per cent, according to auction results released by the Monetary Authority of Singapore on Thursday (Apr 25).

This compares with the 3.75 per cent offered in the previous six-month auction, which closed on Apr 11.

Demand was down in the latest tranche. The auction received a total of S$14.4 billion in applications for the S$6.6 billion on offer, representing a bid-to-cover ratio of 2.18.

Eugene Leow, senior rates strategist at DBS, noted that the cut-off on the six-month T-bills seems to be stabilising around the mid 3.70s.

“Market participants would be closely watching next week’s Fed meeting to get guidance on policy direction,” he said.

In comparison, the previous auction received S$16 billion in applications for the S$6.3 billion on offer.

Start and end each day with the latest news stories and analyses delivered straight to your inbox.

Around 96 per cent of non-competitive applications, totalling S$2.6 billion, were allocated.

As for competitive applications, around 21 per cent at the cut-off yield were allotted. Those who specified a lower yield were fully allotted, and those who specified a higher yield were not allotted.

T-bill yields hit a 30-year high of 4.4 per cent in December 2022, and have mostly hovered around the 3.7 to 3.8 per cent range since March 2023, amid the high-interest-rate environment.

While markets were initially looking forward to more rate cuts this year, they have since dialled back on expectations due to persistently high inflation figures in the US.

Already a subscriber? Log in

Recommended

Save 50% for the first year

No lock-in contract

Gift BT stories to non-subscribers

Unlimited digital access to BT premium articles

Catch up on news with our 2-week e-paper archive

Access to our Property, ESG and Garage newsletter archives

Exclusive offers on SPH Rewards at rewards.sph.com.sg

Personalise your reading experience with up to 30 keywords via myBT

'/%3e%3cpath%20d='M35.1847%2014.0422L9.37867%2024.1703C8.88772%2024.363%208.86989%2025.051%209.35015%2025.2688L15.0551%2027.8567C15.2097%2027.9269%2015.327%2028.0594%2015.3778%2028.2212L17.8255%2036.0078C17.9491%2036.4009%2018.4247%2036.5534%2018.7539%2036.3054L23.0143%2033.0968C23.2178%2032.9435%2023.4961%2032.9364%2023.7072%2033.0787L30.8526%2037.8975C31.2091%2038.1378%2031.6951%2037.9339%2031.7732%2037.5114L35.9896%2014.7059C36.0747%2014.2456%2035.6206%2013.8712%2035.1847%2014.0422Z'%20fill='%23FDFEFF'/%3e%3cpath%20d='M15.3125%2027.9998L30.4162%2018.627L19.3691%2029.3628L19.548%2033.3966L18.9531%2036.1248C18.3783%2036.7236%2017.9297%2036.2772%2017.8477%2036.0662L15.3681%2028.178L15.2734%2028.0233L15.3125%2027.9998Z'%20fill='%23C8DAEA'/%3e%3cpath%20d='M18.3594%2036.4259L19.3511%2029.3447L23.519%2032.9856C23.303%2032.9612%2023.1588%2032.9863%2023.0268%2033.0859L19.0712%2036.0718C18.6289%2036.4572%2018.4297%2036.4455%2018.3594%2036.4259Z'%20fill='%23A9C9DD'/%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear'%20x1='33'%20y1='7.5'%20x2='19'%20y2='36.5'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231E96C8'/%3e%3cstop%20offset='1'%20stop-color='%2337AEE2'%20stop-opacity='0'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

BT is now on Telegram!

For daily updates on weekdays and specially selected content for the weekend. Subscribe to t.me/BizTimes

Get the latest coverage and full access to all BT premium content.

SUBSCRIBE NOWBrowse corporate subscription here

SPH MEDIA DIGITAL NEWS

MCI (P) 064/10/2023 © 2024 SPH MEDIA LIMITED. REGN NO. 202120748H

We live in an age with an ever-expanding – and often bewildering – range of investment options, yet the top choice for many young and older folk now turns out to be the humble, dull but dependable fixed deposit.

The finding, which comes in the wake of rising interest rates in the last couple of years, is unusual because about 80 per cent of investors of all ages, including those in the 21 to 30 age group, have such accounts.

Many younger investors used to avoid parking any money in fixed deposits, let alone put the account as one of their preferred “investments”.

Although respondents also prefer government bonds and special savings accounts that offer higher rates on the first $100,000, the fixed deposit is likely to be the dominant product because everyone knows how it works and bank customers can also move their funds into such deposits online.

The ease of making online transactions also signals changes in share investing, noted the Fullerton Fund Management survey, which polled 500 investors who had $40,000 to over $500,000 to invest.

For instance, the numerous online trading platforms appear to have attracted many investors here to dabble in overseas stocks, especially popular technology stocks in the United States, such as Tesla, Nvidia and Apple.

Such stocks are known to be highly volatile in their price swings, and the survey highlights a worrying trend that 60 per cent of investors here do not have investment portfolios that are well diversified.

By signing up, I accept SPH Media's Terms & Conditions and Privacy Policy as amended from time to time.

This means that some of them could be heavily invested in just one stock and thus face higher risk if the value of the stock plunges.

It is clear from the poll that financial literacy is often a work in progress, with many people saying that they cannot rely on property and the CPF – two popular asset classes that many swear by – for retirement.

This feeling was particularly apparent among two age groups – those between 31 and 40, and the 51 to 60 group.

It is possible that investors in the younger group are all too aware of soaring condominium prices in the last few years, making it harder to buy or upgrade to a private property without wiping out most of their savings.

For the older group, it is common for many home owners to end up with smaller CPF balances if they use it to service their home loans.

These owners should know that the most important feature of CPF is not dependent on their fund balance alone but how much they are willing to save for CPF Life, when the national annuity scheme kicks in for those who reach 55.

Indeed, in February 2024 – a few months after this survey was done – CPF Life was given a major boost to allow members to have the option to save more so that they can receive up to $3,300 a month from age 65.

This can be achieved if people who turn 55 in 2025 or older make it their target to top up their Retirement Account in lump sums or in stages to hit the new enhanced retirement sum of $426,000.

As most participants in the Fullerton survey saw the importance of reaping continuous passive income in retirement, the idea of having about $3,000 a month is certainly worth planning for.

After all, in just 10 years, you would have received $360,000, and $720,000 in total by age 85.

Here are some planning tips for three asset classes highlighted in the survey.

Many high-salary earners are content to let their income accumulate in savings accounts without doing anything with it. But if they do not bother to keep excess cash in fixed deposits to earn higher interest, they are in effect missing out on the extra cash from the bank which can fund their holidays.

While a fixed deposit allows your savings to earn more without any risk, you should never view it as your main retirement plan unless you have plenty of cash to begin with.

For instance, even with a 3 per cent rate, you would need $1 million just to earn $30,000 annually, or about $2,500 a month.

Your “earnings” per month would drop considerably to $1,250 if your fixed deposit is $500,000, and $250 if it is $100,000.

Moreover, it is hard to make long-term plans because the interest rate is never stable and changes quite often in tandem with the global economy.

When the rates drop, those who rely on fixed deposits for their expenses will need to dig into the principal sum, which heightens the risk of not having enough money when they are older.

“Don’t put all your eggs in one basket” is timeless advice for investors because many products that promise higher returns are inherently more risky. For instance, if you invest in the shares of only one company, you will sink or swim according to its fortunes.

Most financial planners would never advise their clients to do this simply because if they pick the wrong investment, they will be wiped out if that company’s shares are suspended indefinitely due to business failures.

Even if you invest in only reputable companies, you should be mindful of your goals.

While younger investors can afford to take a long-term strategy and weather the ups and downs of price swings, retired investors cannot.

Unless the stocks they pick pay decent dividends, holding shares alone will not pay your expenses unless you cash out.

Retired investors face more risk because if stock values are down and they need money to pay the bills, they may be forced to sell at a loss.

People who put money into investment funds face similar situations.

So before signing up for any, check if the fund pays returns regularly or if you will get cash only when you terminate your deal in full or partially.

Find out the procedures for termination and whether there is a minimum lock-in period. Ask also about the management costs because costly products will naturally mean your investment is only profitable if the returns are much higher.

Don’t be shy in asking even the most basic questions because there is no such thing as a dumb question when it concerns your money. It is better to be clear about everything before you part with your funds than be sorry when you are hit with losses later because you were ignorant of the risks.

After investor confidence was pummelled repeatedly with news of fraud and market manipulation in the last two years, many people steered clear of such assets.

The Fullerton survey found that cryptocurrency ranked the lowest in terms of investment choices, after corporate bonds, mutual funds, unit trusts, shares, government bonds and fixed deposits on top.

After seeing batches of crypto investors being burned, many investors polled said they chose to “focus on achieving long-term financial security and prioritising steady gains over quick profits”.

This is a wise move because anyone planning for retirement can ill afford to put money in super risky products that can wipe the slate clean. If you can’t stomach any investment losses, stick to safe haven assets like fixed deposits and government bonds that will not cause you to lose any sleep.

Join ST's Telegram channel and get the latest breaking news delivered to you.

")

字体大小:

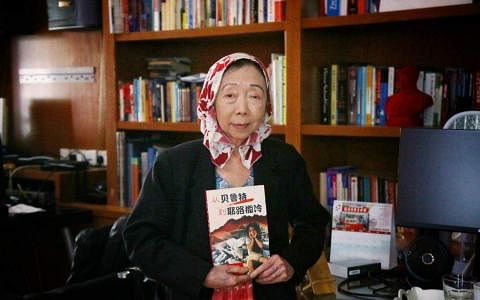

约四年前从香港移民新加坡,并设立家办Paeonia集团的女富豪洪燕,有一段颇为传奇的人生经历。

她的父母原为中国物理学和化学研究员,却因文革举家迁到香港,从烧焊和车衣等底层工作做起。洪燕一度得当童工来支援家庭。后来,她考入美国宾夕法尼亚大学沃顿商学院,毕业后成为投资银行雷曼兄弟的业务分析师。

当事业蒸蒸日上时,她辞去稳定的工作,全身心投入到中国经济起飞的大势。从1990年到2015年,她将母亲的分析仪器贸易业务扩大,赚得了人生的第一桶金,还在中国购置了100多套房产。

本期“早人物”访问洪燕,看她是怎么从女童工走向女富豪、她投资与事业路上的人生感悟,以及她与新加坡的渊源。

去年4月,一名神秘买家以3558万元向凯德腾飞房地产信托(CapitaLand Ascendas REIT)收购位于甘榜安拔(Kampong Ampat)的一栋工业大厦,出价比项目2022年底的估值高出55%,更比凯德腾飞2005年购买的价格多出两倍以上。

这一交易立即引起了市场的瞩目,也激起了人们的好奇心:这位神秘买家究竟是谁?是什么来头?

她,正是来自香港的女企业家——洪燕。

洪燕是一名资深企业家和风险投资人,约四年前从香港移民到新加坡,并加入创办家族理财办公室的浪潮,在新加坡设立家办Paeonia集团。

除了制造和销售测试设备以及进行各种投资项目外,集团也设立基金会,支持教育、艺术、医疗和社区发展等。

与洪燕面对面接触时,这名女富豪没有高高在上的姿态,给人的印象平易近人,谈话诚恳且积极向上,不时有着精辟睿智的人生感悟和金句。她做起事来也显得低调而不张扬,没有许多新晋富豪的炫富或奢侈作风。

她接受《联合早报》专访、谈起她的成功事业时,只说自己是幸运地抓住了百年难得一遇的“中国顺风”机遇。自己人生目标,从来不是要成为女富豪,要赚很多很多的钱。

洪燕说:“我想有个精彩人生,繁花似锦,有着心里面的平安喜乐。这个心里面的平安喜乐,是因为你看见的人都有张高兴的笑脸。我觉得,当你看见别人高兴,你就能够高兴,那你也就能真正地找到心里面的平安喜乐了。”

她从凯德腾飞房地产信托买入的工业大厦,主要是自用。“我们不是要炒卖房地产,只是把房地产作为主要资产配置。”

最近,她看中另一栋工业大楼,但与投资团队商量后,后者建议这项目可能不太容易租出去,存在较大的投资风险。

“但我觉得,如果这地方不好租,我们就把它改建成社区中心,让附近的孩子来这里读书或打打游戏机,这也是不错的啊。”

对她而言,收购工业大厦将可能是她搭建社区中心的第一步。她的人生,已经经历了若干次的低谷和高潮,现在进入到回馈社会、泽被后世的新的人生境界。

事实上,洪燕一直积极回馈社会,特别是教育科研方面。

今年2月,Paeonia基金会南洋理工大学捐赠500万元,用于支持与宾夕法尼亚大学合作的领导力发展计划,并设立新的教授职位,以吸引全球顶尖人才。洪燕本身也是南大董事会成员。

2022年,她资助诺贝尔奖物理学家奎洛兹(Didier Queloz)到南大进行公开讲座,分享天文学心得。

作为一名艺术和教育慈善家,洪燕曾支持沃顿商学院、牛津大学、剑桥大学、清华大学、武汉大学、新加坡国立大学,以及香港管弦乐团等多家机构。

她也向飞跃家庭服务中心等社区机构慷慨捐款。

由于她的各种贡献和成就,她被评为沃顿商学院2019年度中国企业家,以及圣马可学校的2013年杰出校友。

积极支持教育科研的洪燕说:“钱不能留住,但教育可以。只要你有本事,跑到哪里你都不怕。”

她当初就是凭着优异学业成绩而脱贫,如今她抱着感恩情怀,也想通过资助教育科研帮助他人。

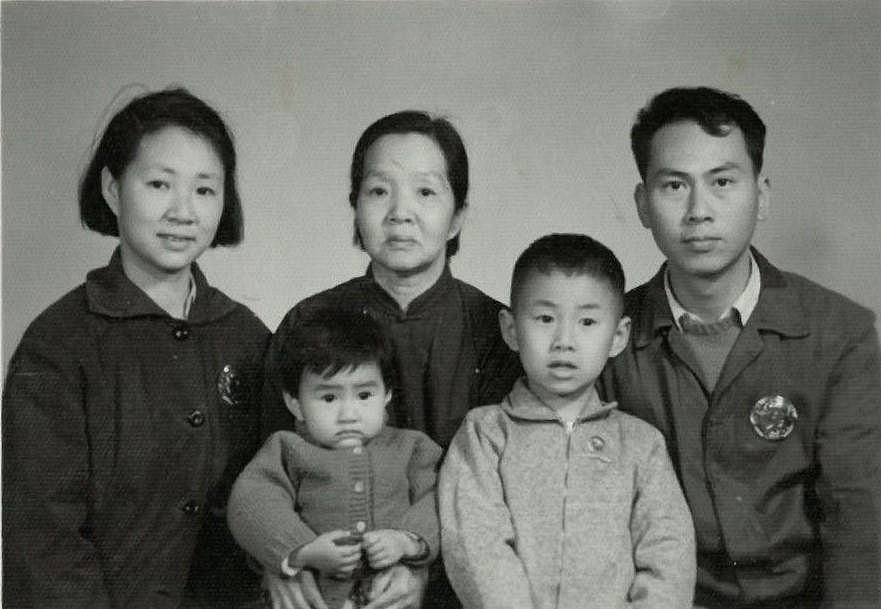

洪燕出生于北京,祖籍漳州,祖上曾有人在当地担任过官职,享有一定声望。

1937年中国抗日战争时期,她的祖上从中国途经新加坡,来到印度尼西亚的泗水,成为早期的印尼华侨。所以,洪燕对南洋有一份深厚感情。移居到新加坡,有一种落叶归根的感觉。洪燕能够说流利的福建话,也懂得一些印尼语(Bahasa)。在新加坡生活时,当她偶尔听到一些人说着与印尼语相似的马来语,或者品尝到印尼美食时,不禁让她有似曾相识的感觉,也勾起她与婆婆在一起时的童年回忆。

1950年代,洪燕的父母洪德炎和杨安钦回到中国发展,分别考入武汉大学的物理系和化学系。

洪燕说,父母原来是备受看好的年轻科研人才,毕业后分配到北京,在中国科学院和石油部担任研究工作。但时代的打击往往来得措不及防,遇上文化大革命,全家被下放到湖北钱江的农村干校。

在洪燕六岁时,父母决定带着她与哥哥以及外婆,举家迁移到香港生活。昔日科学家,被迫沦为工厂工人。

洪燕指出,父母虽然是科学学者,但不会说广东话和英语,而且他们在武汉大学获得的学位并不被香港政府和企业承认。

因此,他们只能从基层工作做起,父亲做焊工,母亲做缝纫工,她和哥哥放学后帮忙家务做家庭工,贴补家用。

洪燕回忆道:“我们一家住在荃湾,房子只有80平方英尺……小时候,我们连港币30元(约5新元)的幼儿园学费也付不起。我记得妈妈带我去坤慈幼儿园,但由于学费太贵,只好带我回家。因为洗澡得要用煤油炉烧水,所以每周只能洗两次澡。因此,我学会了节约时间,三分钟洗完澡,五分钟吃完饭,把时间用在更有用的事情上,比如读书和做家务。”

她带着一丝苦笑说,小时候做的童工是给玩具娃娃穿衣服,“但我从来没有自己的娃娃”。

洪燕对于“大快活”(香港连锁快餐店)的炸鸡腿饭印象深刻。因为在小学四年级,她拿到全班第一名后,父母带她去那里庆祝。“那是我第一次尝到炸鸡腿饭,我才发现原来大快活有如此美味的食物。”

尽管家境贫寒,洪燕从来不抱怨父母。她说:“穷与富是相对的。当时我们家和楼上楼下的邻居都穷,所以我从不觉得我们很穷,相反地,我觉得这样的生活挺好。有时一家人聚在一起吃饭,可以有一碟红烧肉,我们已经很快乐。我对小时候的生活没有怨言,反而认为这是父母给我的最好礼物,让我从小学会独立面对困难。”

约1980年代,随着中国的改革开放,洪燕的父母开始找到更多的工作和商业机会。这时,洪燕也迎来了人生的一个重要转折点——她成功申请到美国读高中。

洪燕从小学业成绩优异,经常考全年级第一名。小时候,她有许多梦想,喜欢武侠小说的她曾梦想成为女金庸,父母则希望她成为科学家,像“居里夫人”一样。然而,她的梦想只有一个,就是去她向往的美国求学,一心想要考上享有盛誉的哈佛大学。

尽管数学和物理成绩优异,但她未能进入哈佛大学,而是被宾夕法尼亚大学录取,毕业于沃顿商学院。

值得一提的是,大约在1990年毕业后,洪燕加入了当时备受瞩目的投资银行“雷曼兄弟”,成为一名投资银行员工。然而,洪燕只在那里工作了七个月,在听了一场香港和记黄埔前董事总经理、外号“和黄大班”的马世民谈中国前景的演讲后,她毅然辞职,回中国创业。

四年后,她如愿以偿被哈佛大学录取。仅仅三个星期后,她再度放弃别人眼中的黄金机会,义无反顾回中国继续刚创下的事业。

1990年,正值天安门事件发生约一年多,中国正处于低谷,经济衰退、人口增长、资源枯竭以及国际孤立等问题接连不断。然而,对于洪燕来说,中国的危机可能是她最好的人生机会。

她说:“当社会出现任何巨大变化时,机遇总是随之出现。我始终看好中国,全心投入中国发展,相信它未来会迅速崛起。如果我还继续留在雷曼或哈佛,将会错失这个千载难逢的好机会。”

事实证明,洪燕的决定正确,她牢牢抓住1990年至2015年中国经济起飞的关键时机,成为赶上大潮的勇者。

短短几年内,洪燕在母亲的分析器贸易业务的基础上,创立了环球(香港)科技有限公司(Universal (Hong Kong) Technologies),经销科学测试和分析仪器。随后,她又设立CFR Engines Group,生产燃料测试设备等。这让她赚到人生第一桶及后来的很多桶金。

除了经销和生产测试设备,洪燕相信“有土斯有财”,在中国投资买了100多套房产。她的投资策略是在国际学校附近购买洋房出租,在地铁沿线的中央商业区买办公室。这些房产大部分在2018年前后已经卖出,给洪燕带来可观的回报。

谈到她的房地产投资收益时,她笑说:“如果以前一平方米的地相当于摆满Gap包包的总值,那么2018年时它们的价值已经升值到香奈儿,甚至爱马仕的名牌包了。”

约四年前,洪燕决定移民新加坡。她对新加坡良好的教育系统和稳定的社会环境印象深刻,同样也看好新加坡投资前景。

洪燕说,她的目标是将公司的业务扩展至全球范围,新加坡作为一个国际性的枢纽,有助她管理这些全球化业务。此外,新加坡蓬勃的创投生态环境,也为她进入南亚和东南亚市场提供了机遇。她就在量子计算、机器学习和生物技术领域的私募股权、风险投资和初创公司进行投资。

她创立的Paeonia集团也参与新加坡创投基金和起步公司投资如禹徽资本(Insignia Ventures Partners)、艾昂动力(Ion Mobility)和Bifrost等。

洪燕有两个孩子,他们分别是15岁和18岁,目前在求学。

许多富豪往往都为如何将企业和财富传承给后代而发愁,白手起家的洪燕却不以为然。她打算透过Paeonia集团的基金会,把自己的大部分财产捐献出去。她认为,这种教育、学术界及社区等领域的捐赠,意义远远大于直系亲属传承财富。

她说:“我们家从有钱到没钱,然后从没钱又活过来。这些人生起落告诉了我,这个世界是充满不确定性,任何时候你拥有的东西,都可能全部失去。你唯一能依靠的就是你自己。你要怎么靠自己呢?那就是勤奋学习,积极向上,然后为行善积德,为世界做好事。因为善有善报,最终你也将得到回报。”

Paeonia是牡丹花的科学名称,所谓赠人玫瑰,手有余香,洪燕希望通过Paeonia集团的回馈捐献,把这善行的花香,传递给每个人。

立即订阅

*无合约